State of the Industry: Vontobel on the Redrawn Watch Market

Macro headwinds and divergent results.

Last month Vontobel published its annual report on the Swiss watch industry, revealing a startling shakeup for the pecking order, with a rapidly growing share of the market going to industry giants, anaemic growth, and a few signs of hope. Another of the key points made in the report published by Vontobel, a family-controlled Swiss private bank, is influence of external factors beyond the industry’s control, like the strong Swiss franc and continuously climbing gold prices, but which have nonetheless played a major role in its recent development.

Long the go-to publication for industry insiders, the Vontobel watch report has been published annually for well over a decade — and since 2021, the report has been authored by Jean-Philippe Bertschy, the bank’s head of Swiss equity research (pictured above).

The strong franc

Before getting into the numbers, it’s worth looking at the broader macroeconomic environment affecting the industry. The strong franc and weak dollar are headwinds for the export-oriented Swiss watch industry, and, like erratic US trade policy and soaring gold prices, entirely outside its control.

In nominal terms, total Swiss watch exports declined for the second year in a row, down 1.7% to CHF25.5 billion, following a 2.8% decline the year before. However, the Swiss franc’s appreciation casts a more sympathetic light on these numbers.

For example, if you sold a watch for US$100 this time last year, that revenue would have converted to about CHF90. Today, however, that US$100 would be worth just CHF78. As a result, Vontobel estimates that “adverse FX has reduced revenues for the major global brands by roughly 10-15% over the past four years, depending on their regional mix”.

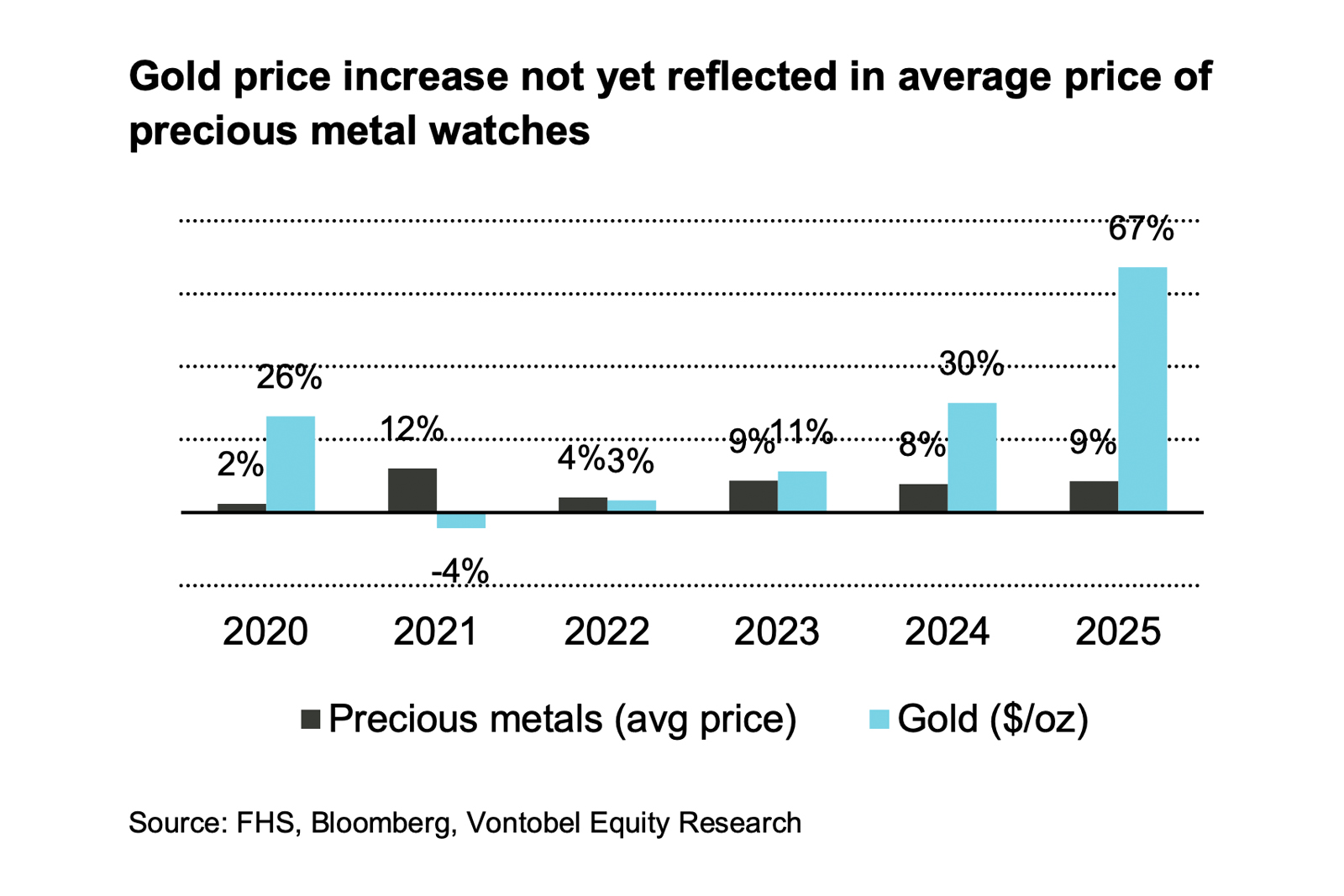

Interestingly, Vontobel notes that most brands chose not to pass along the rising cost of gold, at least in 2025. This is actually one lever that could have alleviated some of the downward pressure on margins, and the fact that brands didn’t feel confident passing this cost along is telling.

This is not the first time the Swiss watch industry has had to navigate these kinds of conditions. In 1971, the collapse of the Bretton Woods system sent both Swiss franc and gold soaring, at the same time Japanese watches (of both quartz and mechanical varieties) were gaining market share. The resulting crisis was the industry’s worst since the 1930s, a period today known as the Quartz Crisis.

Winners win more

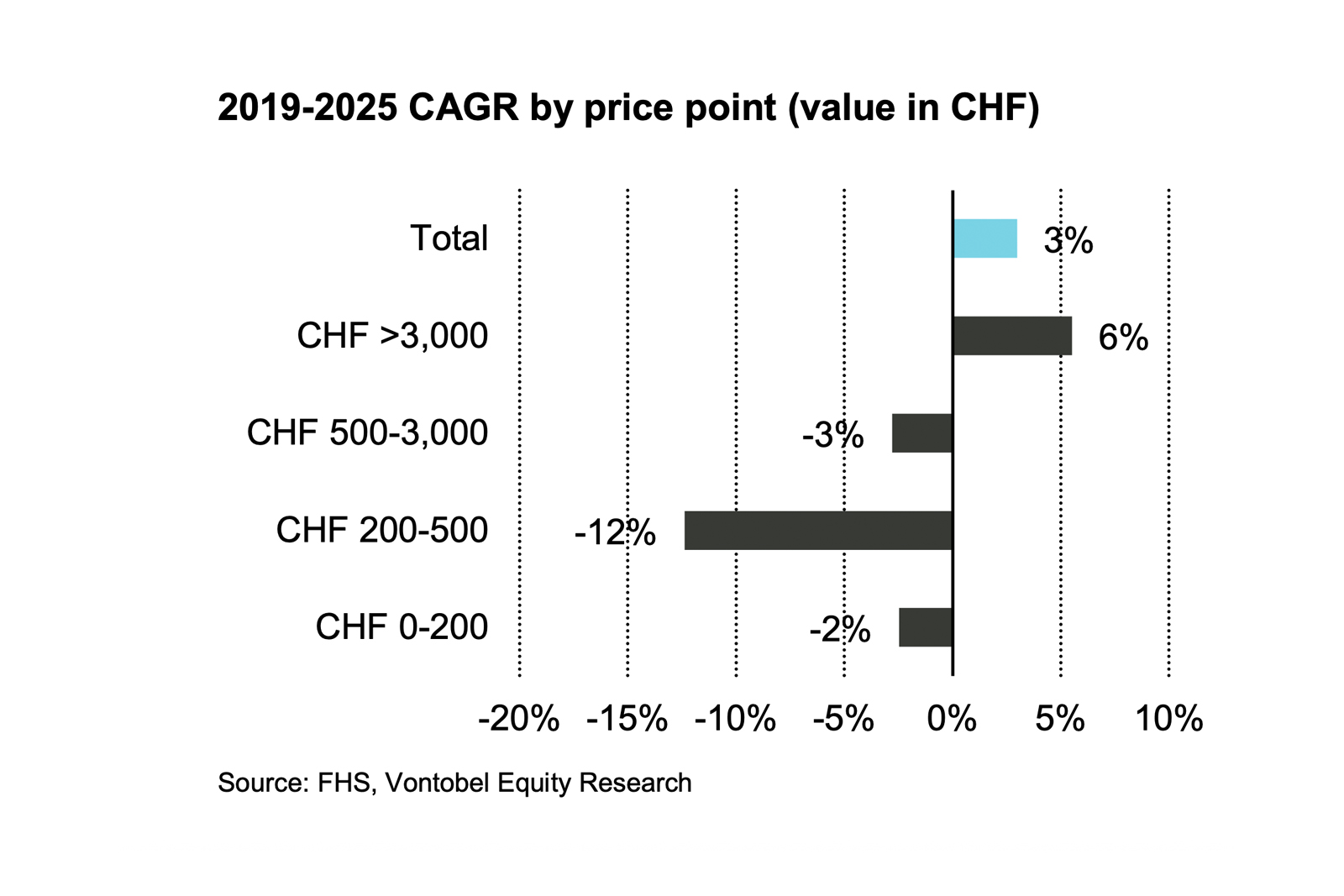

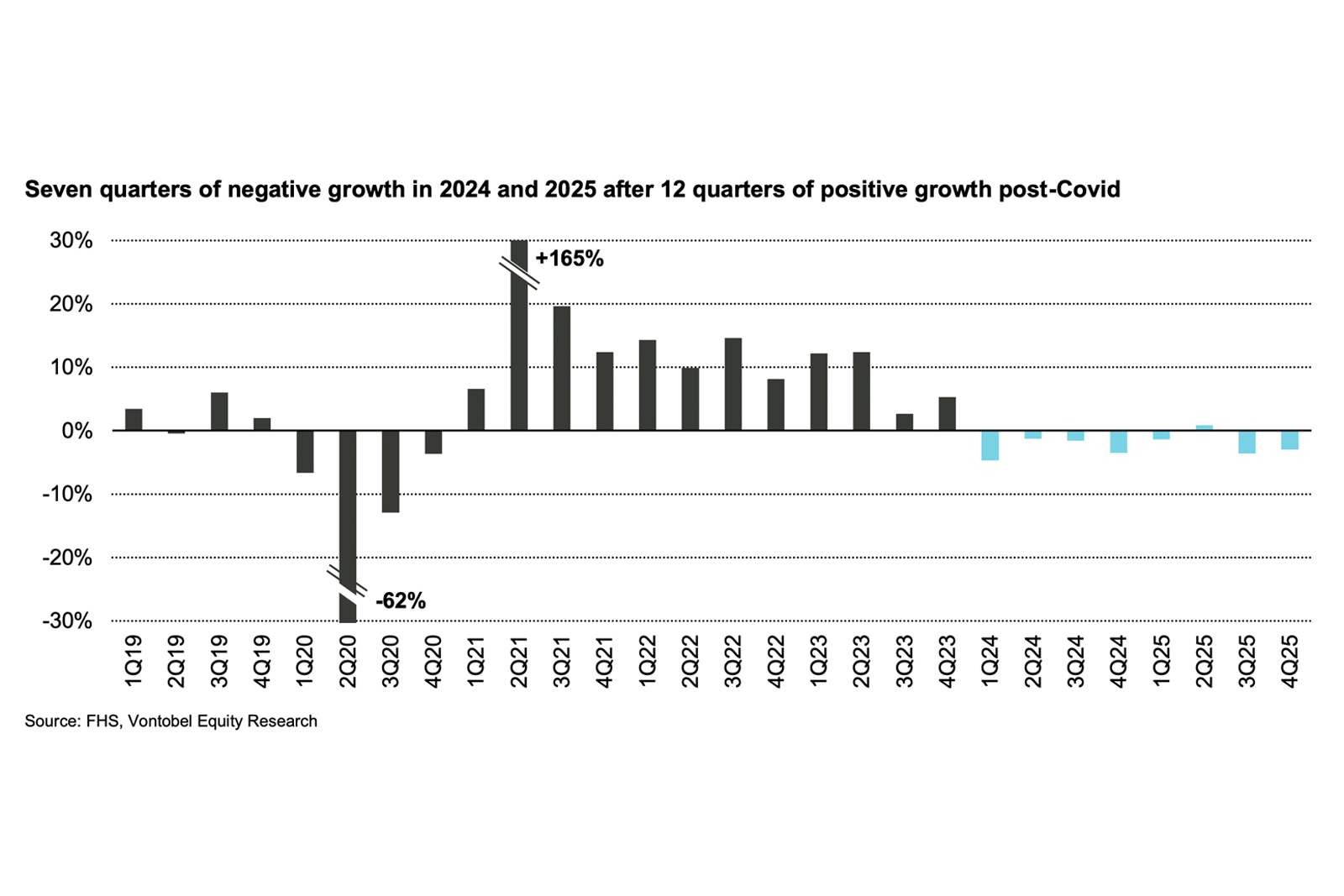

Looking at the market as a whole, the familiar K-shaped divergence in Swiss watch demand continued in 2025, with growth concentrated at the top of the market and contraction at the bottom. The ultra-luxury segment — defined as watches priced above CHF20,000 — continued to expand, while the entry-level sub-CHF500 segment shrank by 4%.

More surprising was the performance of the mid-to-upper tier. The luxury segment, defined as watches with ex-factory prices exceeding CHF3,000, contracted by 1.9% after eight consecutive years of growth. The CHF500-3,000 bracket, home to brands like Tudor and Longines, eked out a marginal gain of 0.2%.

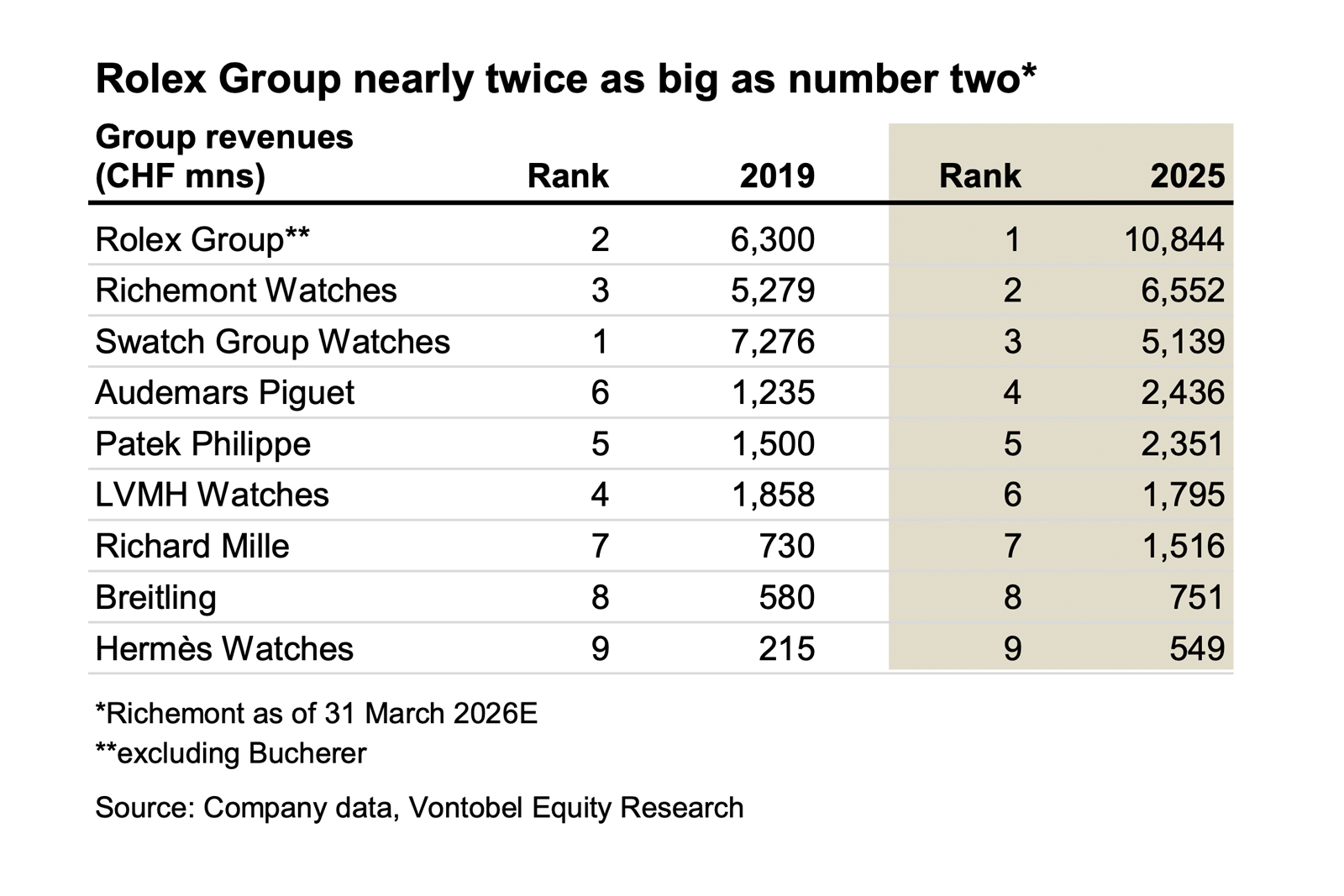

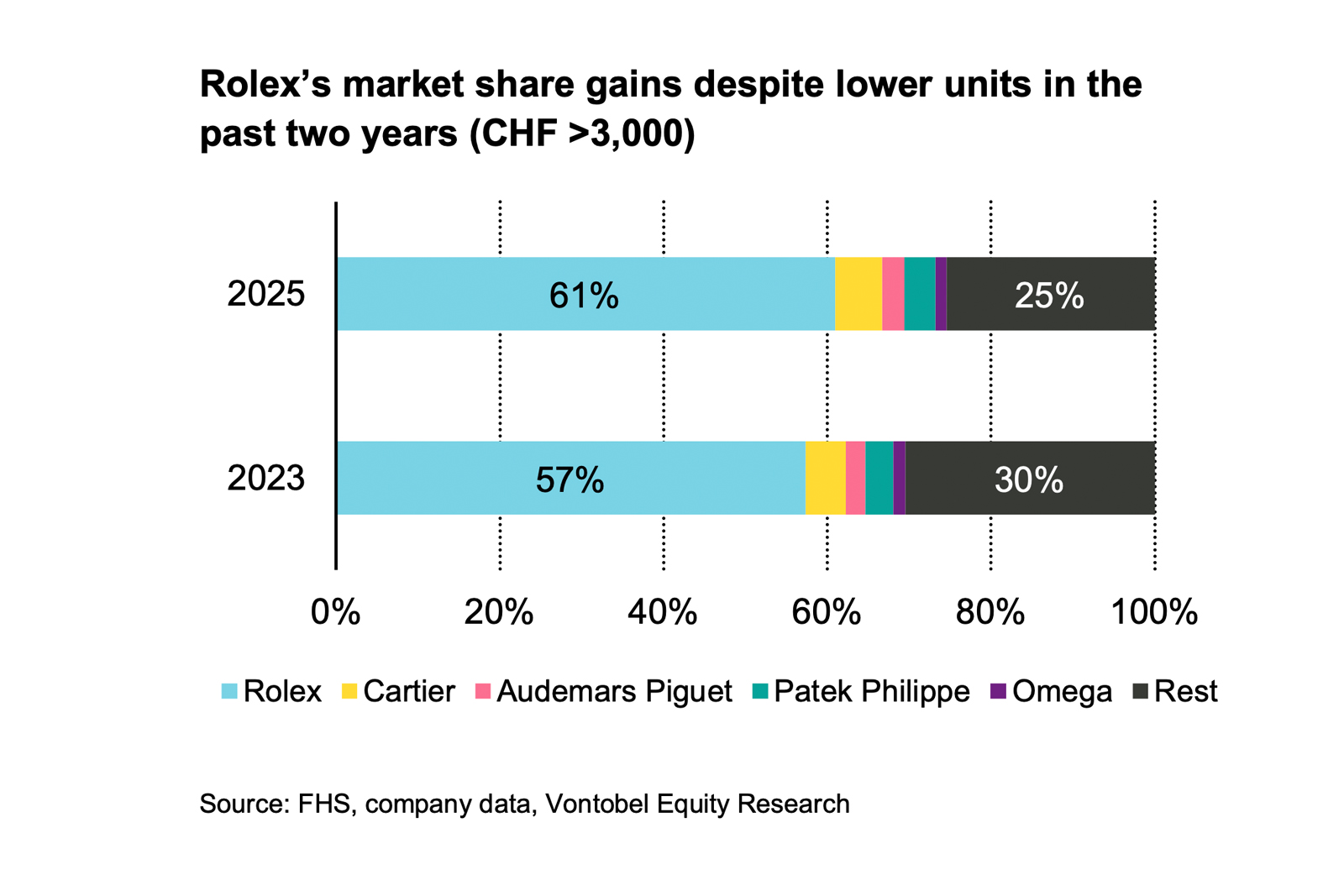

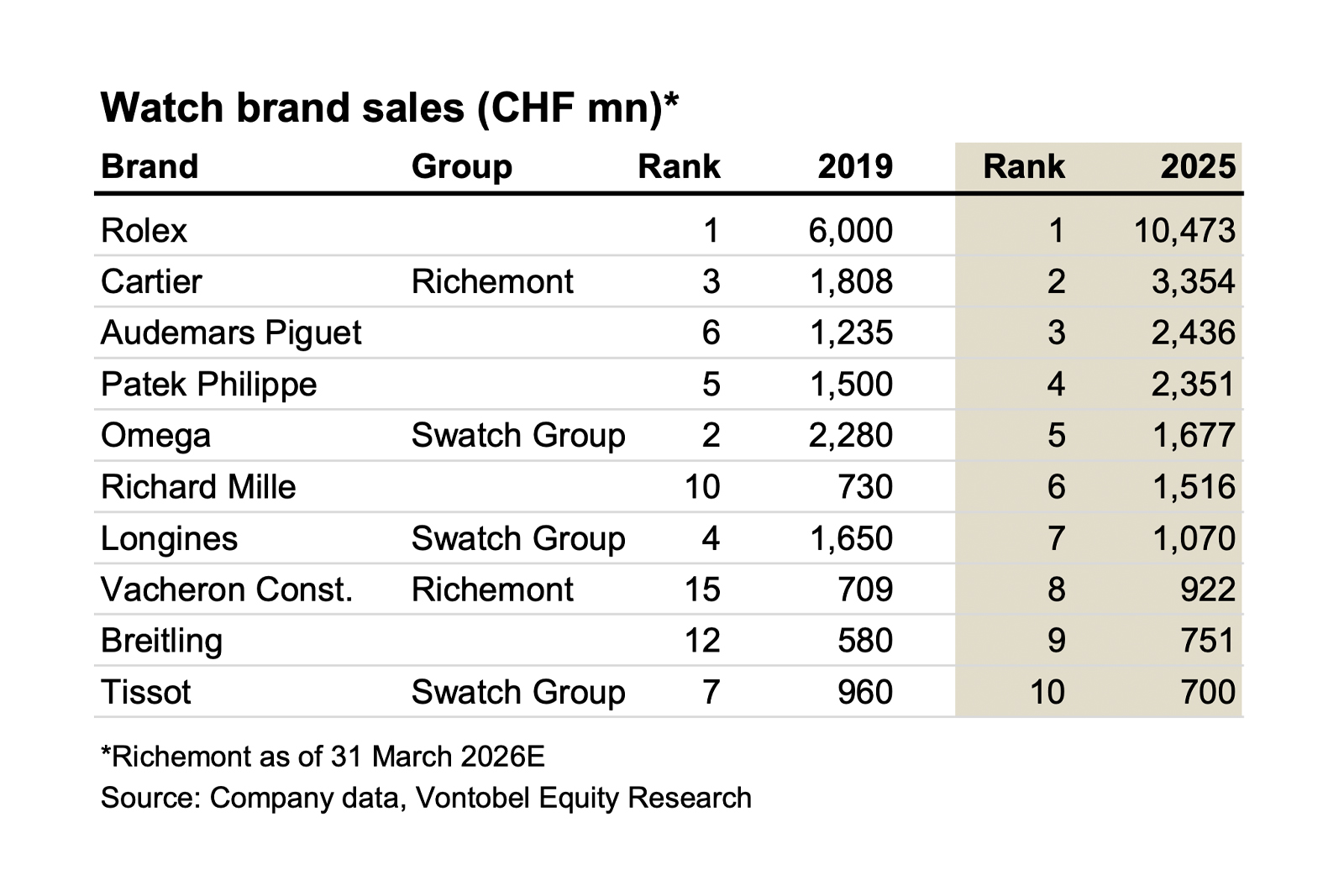

Zooming in past the segment-level analysis, the success of Rolex and Richemont’s Cartier continued. Rolex was buoyed by its certified pre-owned programme (CPO) in particular, which generated CPO after-sales service revenue on more than CHF500 million in sales last year. Treated as a standalone brand, Rolex CPO is larger than Tudor.

Like Rolex, Cartier has unique brand and pricing power, and strong interest from both men and women. Unlike Rolex, it can lean on its branded jewellery business, which is the largest in the world and was phenomenally successful last year.

Interestingly, Vontobel believes that following years of growth, Rolex cut production for the second time last year. The bank posits that this was voluntary, done to maintain pricing power and related to the growth of the CPO program.

Those factors might well explain the decrease in production, but the industrial transition to production of the revolutionary cal. 7135 may also have reduced absolute numbers. Perhaps Rolex’s launches this year will shed more light on this.

Moving up to the ultra-luxury price bracket, Audemars Piguet and Patek Philippe grew revenue without increasing units sold. This was a consistent theme across the market; among the top 10 brands by revenue, only Cartier and Richard Mille managed to move more merchandise, on a unit basis, than the year before.

A wholesale-istic view

It is important to point out that these numbers represent the brands’ turnover, not the total value of watches sold to consumers, a nuance often glossed over in coverage of these reports.

For example, the total retail sales value of Patek Philippe likely exceeds that of Audemars Piguet, despite ranking behind its rival from Le Brassus in Vontobel’s revenue analysis. However, like Rolex and most other brands, Patek Philippe primarily sells watches wholesale to regional distributors, who then sell on to authorised dealers, which get a sizeable cut of the action. Crucially, however, Rolex and Patek Philippe own most of their regional distribution.

In contrast, Audemars Piguet has terminated much of its authorised dealer network and now sells watches directly to consumers, capturing the retailer’s margin for themselves. There are still third parties involved occaisionally, such as Material Good that help operate boutiques and “AP Houses”, but fundamentally it’s a direct-to-consumer model. This results in greater revenue, but also greater costs – and only the former shows up in these reports.

For this reason, Vontobel’s report points out that top-line revenue figures are not fully comparable. Interestingly, this nuance suggests that Rolex’s lead over the second largest watch brand, Cartier, may be even bigger than it first appears, since Cartier generates a larger share of its sales through its own boutiques.

The world’s largest Rolex boutique is operated by Ahmed Seddiqi. Image – Ahmed Seddiqi

Assuming a conservative average retailer margin of 30%, total sales of Rolex watches to end consumers is likely in excess of CHF15 billion. The figure cited by the Morgan Stanley watch report is a comparable CHF16 billion.

On that note, Swatch Group once again pushed back against the veracity of the Morgan Stanley report’s conclusions, which differ substantially from those provided by Vontobel. The two banks diverge most strikingly on Omega, where Vontobel’s figure is 24% lower, and Longines, where it is 16% higher.

Alpha and Omega

Swatch Group’s open letter criticising the Morgan Stanley report danced around Omega’s significant downturn, which was noted in both reports, only pushing back on its relative ranking, not its turnover.

The letter mentions Vontobel by name but stops short of criticism, suggesting the bank’s estimates for Omega and Longines may be close enough to withstand protest. If that’s the case, it paints a bleak picture for Omega, and marks a definitive end for Omega’s position as the second largest Swiss watch brand, something many once took for granted.

During the mid 1990s, Swatch Group rallied around Omega as its champion in the luxury space and set about rebuilding the brand to take on Rolex. This effort was ultimately successful, and the brand’s turnover passed the nine-figure mark during the 2000s, driven disproportionately by the emerging Chinese consumer market. Swatch Group’s 2007 annual report even describes Omega as the “undisputed market leader” in this critical market.

By 2019, Omega had entrenched its position as the second largest watch brand by revenue with about CHF2.28 billion in sales against Rolex’s CHF6 billion. However, the brand’s exposure to China, which led to its growth, left it extremely vulnerable to the post-COVID Chinese consumer slowdown.

Since then, Rolex’s turnover has grown every year, reaching CHF10.47 billion last year — a 75% increase. In contrast, Omega’s sales have declined 26% to CHF1.677 billion today, a fate which Vontobel attributes to the brand’s exposure to China and unfocused catalogue.

This risk didn’t come out of nowhere. As far back as 2012, Richemont Chairman Johann Rupert famously said during a conference call with investors, “I feel like I’m having a black tie dinner on top of a volcano, okay? That volcano is China.”

It is also worth noting that Omega’s gross margins are unknown. On the one hand, the margins might be tighter than those of the other brands in the top five, since Rolex, Patek Philippe, and Audemars Piguet can find margin through greater pricing power, while Cartier is likely able to keep costs down thanks to its more economical approach to watchmaking. But on the other, the impressive industrial base of Omega’s parent, Swatch Group, might allow it to produce quality watches at costs unmatched across the industry, with the sole exception of Rolex.

Omega is caught in the middle, committed to making technically advanced movements without the pricing power to benefit from it, at least for now.

The sky isn’t falling

Despite the downward trend seen throughout much of the report, there may be a light at the end of the tunnel for Omega and other brands with significant exposure to the Chinese market, with Vontobel reaffirming the recovery in China already seen in other luxury segments. In fact, Vontobel recommends its clients maintain their positions in Swatch Group.

Additionally Vontobel sees Richemont – which saw a small contraction in sales by its specialist watch brands but massive growth from its jewellery houses last year – as undervalued.

While not mentioned by Vontobel, sustained near-zero Swiss inflation is another mitigating factor, and on the manufacturing side, key industrial inputs like electricity were actually cheaper in 2025 than 2024, which Swiss government power regulator ElCom predicts will continue into 2026.

Back to top.